CCR Simulation

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

Counterparty risk is the risk that the counterparty to a financial transaction may fail to meet its contractual payments, causing financial loss for the bank. The risk will be incurred in the event of default by a counterparty.

If one party of a contract defaults, the non-defaulting party will find a similar contract with another counterparty in the market to replace the default one. That is why counterparty credit risk sometimes is referred as replacement risk.

Counterparty credit risk is measured by credit exposure. Credit exposure is generated by pricing all deals into the future under Monte Carlo simulation and aggregating using all relevant netting and collateral agreements.

Simulation of credit exposure dates back to the mid-1980s. Early analysis focused on individual interest rate swaps and FX transactions, and was designed to provide an empirical basis for the parameters in what came to be known as the mark-to-market plus add-on approach. In the early days, application of netting was not legally certain. Thus, the simple addition of assessments for single transactions did not introduce a serious distortion.

As netting (Master Agreements) became more widely recognised in markets, some means of reflecting this risk-reducing phenomenon in credit assessments became more urgent. The mark-to-future solution became popular. Under this solution, potential future exposure to a counterparty is measured by evaluating existing trades with potential future market prices over the lifetime of the existing transactions. The exposure (mark-to-future value) is the amount that the bank would lose if counterparty default at that future date. Normally, simulation in this framework does not take counterparty default into account and also assumes that counterparty credit quality and market factors are independent.

Wrong way risk occurs when exposure to a counterparty is adversely correlated with the credit quality of that counterparty, while right way risk occurs when exposure to a counterparty is positively correlated with the credit quality of that counterparty. CCR that needs to take wrong/right way risk into account is calculated in a real world probability measure.

The simulation mode is also called conditional-on-default simulation. The goal of conditional-on-default simulation is to generate correlated random drivers. These correlated random drivers enable counterparties and market risk factors have dependency on each other.

In order to compute exposure at default, ideally we need to simulate a counterparty’s default and correlate the creditworthiness of the counterparty with market risk factors. Then we only calculate the implied exposure if a default has occurred. Given the rarity of a default it would often be necessary to generate a million or more full market scenarios to obtain as few as a thousand instances of default.

The obvious problem with this “brute force” approach is that it is massively wasteful of computing resources. In the overwhelming majority of instances, for all but the shakiest of counterparties, there will be no default. In these cases the exposure amount is irrelevant to the credit exposure since no default occurs.

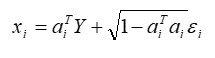

Since the number of counterparties could be thousands, it is unrealistic to simulate each of them. Instead, we simulate some credit indices. Let X_i be the log-solvency ratio of counterparty (or reference entity) i, given by

where the vector a_i is the weighted correlation coefficient that reflects the effect of the credit indices on counterparty/entity i, e_i is the idiosyncratic risk for counterparty/entity i, the vector Y is the credit indices, where each element of Y and e_i are independent standard normally random variables.

The survival probability of counterparty/entity i is given by

| Related Topics |