CCR

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

Counterparty credit risk (CCR) refers to the risk that a counterparty to a financial transaction may fail to fulfill its contractual obligation causing financial loss to the non-defaulting party. It will be incurred in the event of default by a counterparty.

If one party of a contract defaults, the non-defaulting party will find a similar contract with another counterparty in the market to replace the default one. That is why counterparty credit risk sometimes is referred as replacement risk. The replacement risk is the MTM value of a counterparty portfolio at the time of the counterparty default.

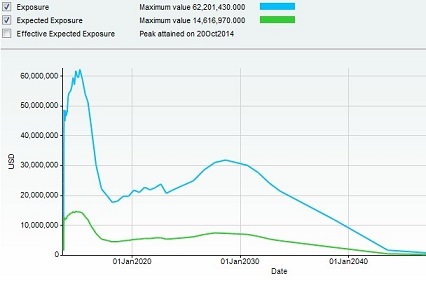

Counterparty credit risk measurement is credit exposure (CE). It is the cost of replacing or hedging a contract at the time of default. The risk is commonly reduced to the peak value of that profile for simplicity. Below is an example of an exposure profile of counterparty X.

The profile above can be interpreted by the following statement: at any point in the future, assuming the counterparty survives up to that point, how much exposure might we have against counterparty X within our entire portfolio with them – and this inclusive of any agreement or collateral that either us or the counterparty might hold. In this case, because of netting benefits and exposure reduction due to a CSA, the peak exposure only rises to 62 MM USD. The blue and the green lines reflect Potential Future Exposure (PFE) and Expected Exposure (EE) respectively.

Exposure is always a positive number; this is because in a default situation, any money owed from the counterparty to the bank may be lost, but any money owed from the bank to the counterparty must still be settled.

CCR relies on exposure profiles. They are the product of pricing all deals into the future under Monte Carlo simulation and aggregating using all relevant netting and collateral agreements. Another important feature that is shared with VaR calculation is the simulation of underlying market factor that is required in order to evaluate those deals; however for CCR the time horizon for simulation is in years rather than days or weeks for VaR.

One key feature is the ability for counterparties to be considered in a state of default at the time of evaluating the portfolio we have against them; this allows positive and negative correlations between exposures and counterparty default to be captured (wrong and right way risk).

In the CCR context, simulation models have the objective to forecast within a reasonable range and horizon market factors such as equity prices, interest and FX rates, CDS curves and so on. In order to capture a realistic view of our exposure going forward, and because CCR is not directly hedgeable, those models are typically calibrated using historical data (~3 years) and are not systematically implied from today’s market prices.

Counterparty risk is much less specific for pricing models than it is for simulating the market prices. The only requirement here is that pricing supports “mark to future” or the path dependent value and events of a trade at any point across the simulation time bucket. This involves storing and accessing reset rates, exercise status, realized stochastic events that will affect our exposure in the future.

Upon availability of the deals pricing paths, aggregation takes place to combine all trades in a manner consistent with the legal netting and collateral agreements to give a single exposure value on each path. From this we evaluate the EE (Expected Exposure) and PFE (Potential Future Exposure); these two measures behave differently as EE corresponds to the average of the simulated exposure and PFE as its 95th percentile.

The end goal of the CCR renewal project is to gain approval for use of the Internal Model Method defined in Basel III. Once achieved, this will create a strong link between the counterparty exposures used for internal risk monitoring and the capital required to be held against that risk.

| Related Topics |