Cap Vol

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

| 1. Cap Volatility Surface Introduction |

An implied volatility is the volatility implied by the market price of an option based on the Black-Scholes option pricing model. In cap market, a cap or floor is quoted by implied volatilities but not prices. An interest rate cap volatility surface is a three-dimensional plot of the implied volatility of a cap as a function of strike and maturity.

The term structures of implied volatilities provide indications of the market’s near- and long-term uncertainty about future short- and long-term forward rates. A crucial property of the implied volatility surface is the absence of arbitrage.

When the implied volatilities are plotted against the strike price at a fixed maturity, one often observes a skew or smile pattern, which has been shown to be directly related to the conditional non-normality of the underlying return risk-neutral distribution. In particular, a smile reflects fat tails in the return distribution whereas a skew indicates return distribution asymmetry. Furthermore, how the implied volatility smile varies across option maturity and calendar time reveals how the conditional return distribution non-normality varies across different conditioning horizons and over different time periods.

The pricing accuracy and pricing performance of option models crucially depends on absence of arbitrage in the implied volatility surface: an input implied volatility surface that is not arbitrage-free invariably results in negative transition probabilities and/ or negative volatilities, and ultimately, into mispricings.

| 2. Volatility Surface Construction Approaches |

To construct a reliable volatility surface, it is necessarily to apply robust interpolation methods to a set of discrete volatility data. Arbitrage free conditions may be implicitly or explicitly embedded in the procedure. Typical approaches are

At FinPricing, we use the SABR model to construct cap implied volatility surfaces following the best market practice.

| 3. Arbitrage Free Conditions |

Any volatility models must meet arbitrage free conditions. Typical arbitrage free conditions are

Vertical arbitrage free and horizontal arbitrage free conditions for volatility surfaces depend on different strikes. There is no calendar arbitrage in cap volatility surfaces as caps with different maturities have different cash flows and are associated with different indices. In other words, they can be treated independently.

| 4. The SABR Model |

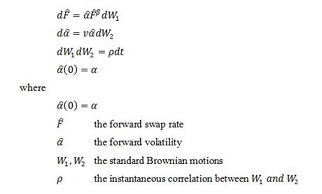

SABR stands for “stochastic alpha, beta, rho” referring to the parameters of the model. The SABR model is a stochastic volatility model for the evolution of the forward price of an asset, which attempts to capture the volatility smile/skew in derivative markets.

There is a closed-form approximation of the implied volatility of the SABR model. In the cap volatility case, the underlying asset is the forward interest rate. The dynamics of the SABR model.

| 5. Constructing Cap Volatility Surface via The SABR Model |

For each term (expiry) and tenor of the cap, conduct the following calibration procedure.

Repeat the above process for each term and tenor.

| 8. Related Topics |