Cap

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

An interest rate cap is an OTC derivative where the buyer receives payments at the end of each period when the

interest rate exceeds the strike, whereas an interest rate floor is a similar contract where the buyer receives

payments at the end of each period when the interest rate is below the strike.

| 1. Interest Rate Caps and Floors Introduction |

An interest rate cap is an OTC derivative where the buyer receives payments at the end of each period when the

interest rate exceeds the strike. It actually consists of a series of European call options

(caplets) on interest rates. The buyer receives payments at the end of each period when the interest rate exceeds the

strike. In return, the buyer needs to pay an up-front premium to the seller.

Interest rate caps are frequently purchased by issuers of floating rate debt who wish to protect themselves from the

increased financing costs that would result from a rise in interest rates. Investors use caps to hedge against the risk

associated with floating interest rate and will benefit from any risk in interest rates above

the strike. The holder gets a payment when the underlying interest rate exceeds a specified strike rate.

An interest rate floor consists of a series of European put options (floorlets) on

interest rates. The buyer receives payments at the end of each period when the interest rate falls below the strike.

The payment frequency could be monthly, quarterly or semiannually. The exercise is done automatically that is different

from any types of options. For example, let the strike be 2.0%. The buyer would get paid if LIBOR fell below 2.0%;

otherwise, he would receive nothing if LIBOR rose above it.

Floors are frequently purchased by purchasers of floating rate debt who wish to protect themselves from the loss of

income that would result from a decline in interest rates. A floor is a guarantee of a future interest rate. Investors

use floor to hedge against the risk associated with floating interest rate. Investors will

benefit from any risk in interest rates below the strike.

| 2. Interest Rate Caps and Floors Valuation |

A cap consists of a series of cash flows, i.e., caplets. Each cash flow is a call option on a floating rate index level at a specified date in future. The price of a caplet is valued using the Back formula. Whereas, A floor consists of a series of cash flows, i.e., floorlets. Each cash flow is a put option on a floating rate index level at a specified date in future. The price of a flootlet is valued using the Back formula.

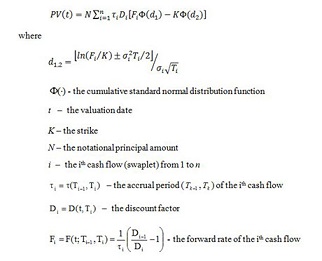

The present value of a cap is given by

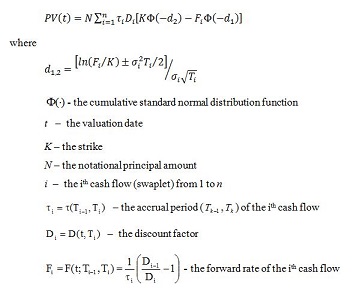

The present value of a floor is given by

Practical Notes

| References |