Lookback Option

FinPricing offers:

Four user interfaces:

- Data API.

- Excel Add-ins.

- Model Analytic API.

- GUI APP.

FinPricing provides valuation models for:

All the equity models in FinPricing take volatility skew/smile and dividend into account.

| 1. Lookback Option Introduction |

A lookback option is a derivative whose payoff depends on the maximum or minimum price of the underlying asset realized before expiry. The payoff is path dependent. There are two types of lookback options: floating lookback option and fixed lookback option.

Floating lookback option compares the minimum or maximum price of the underlying asset achieved to the underlying price at maturity. The strike price of a floating lookback option is not specified at inception but rather calculated at option expiration as minimum for a call or maximum for a put of the underlying asset price over a certain sampling period.

Fixed Lookback Option has a strike price set in advance. The payoff compares the minimum or maximum price of the underlying achieved to a fixed strike price on the expiry date. The payoff of a call lookback option is the difference between the highest value achived and the strike price. The payoff of a put lookback option is the difference between the strike value and the lowest value achived.

Lookback options offers investors an enhanced return and downside protection that “buffers” any negative performance of the Reference Index over the life of contracts

| 2. Lookback Payoffs |

The payoff of a lookback call option on floating strike at maturity T is given by

max ( S(T) - S_min(0,T), 0)

The payoff of a lookback put option on floating strike at maturity T is given by

max ( S_max(0,T) - S(T), 0)

The payoff of a lookback call option on fixed strike at maturity T is given by

max ( S_max(0,T) - X, 0)

The payoff of a lookback put option on fixed strike at maturity T is given by

max ( X - S_min(0,T), 0)

| 3. Lookback Valuation |

The central part of pricing lookback option is to calculate the expectation of the extreme value of the underlying. In general, lookback options with discrete observation have no analytical closed from solution.

Both floating Lookback options and fixed lookback options can have either American or European exercise style. European lookback option can be valued by closed-form formula approximately.

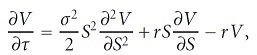

American lookback can only be priced via numerical approach. One advanced solution is to use partial differential equation (PDE). The PDE of a lookback option is givn by

| 4. Related Topics |